Now more than ever, traditional providers are forced to evolve to improve clinician capacity and compete with the tech-enabled alternative care (AC) solutions that rapidly scaled last year.

Although the healthcare industry has seen marked improvements in innovation adoption since 2020, it still lags behind other industries. Historically, tech adoption by providers is slow, hindered by providers resisting new solutions.

Providers must adopt provider operations (PO) solutions to expand consumer-preferred virtual offerings, improve provider workflows, assuage physician burnout and facilitate the adoption of value-based care models.

The pandemic accelerated the physician shortage, leading some providers to adopt PO solutions to expand virtual care options or streamline provider workflows to improve capacity.

Notes: 1) EU includes UK-based companies. Source: PitchBook, SVB proprietary data and SVB analysis.

However, many have lagged in adoption and have alleviated the gap by restricting patient care. Since the pandemic’s onset, over 18% of US hospitals have reduced service hours, and 14% cancelled or delayed elective procedures.1

Subsector: Provider Operations

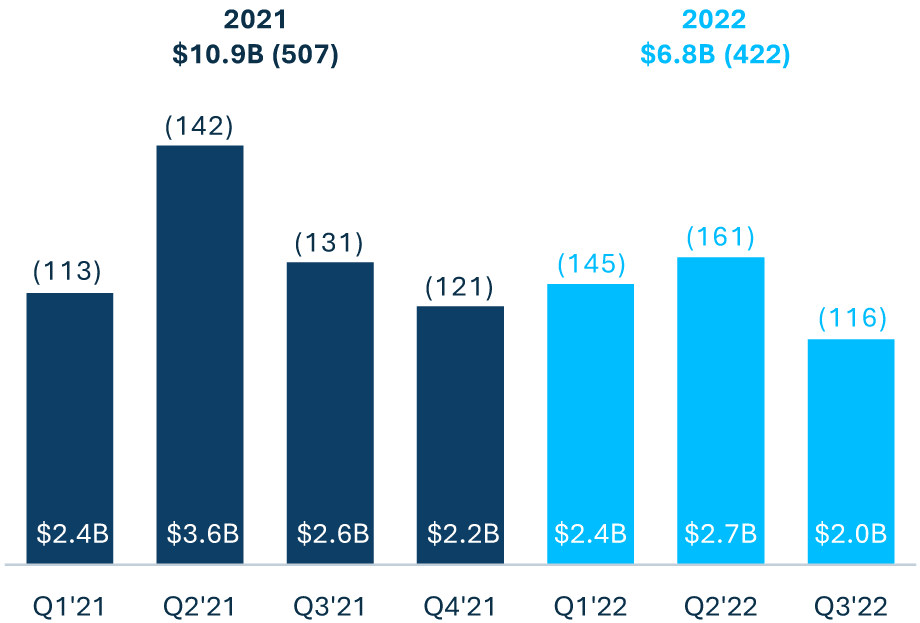

As pressure mounts on providers to adopt technology solutions, investment in PO solutions will remain high. We expect PO to continue to lead healthtech investment in 2023.

2020

2021

20222

Applications

Dollars

Deals

Workflow Optimization

$2.8B

178

$6.6B

284

$4.0B

236

Clinical Decision Support

$2.4B

133

$4.3B

233

$3.0B

188

Notes: 1) Deloitte report. 2) All 2022 data is through 9/30/22. 3) EU includes UK-based companies. Source: PitchBook, SVB proprietary data and SVB analysis.