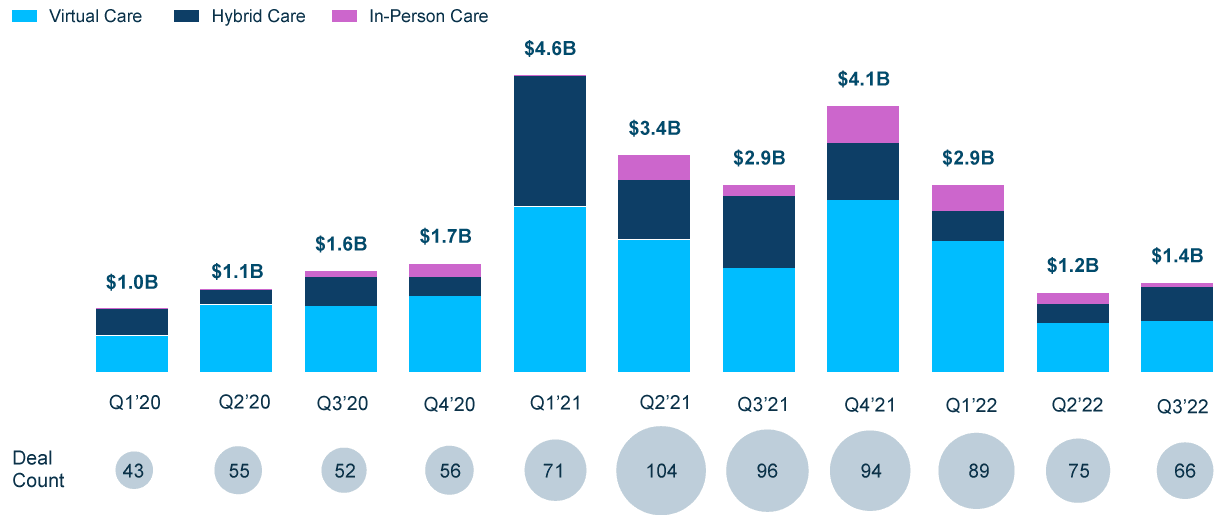

Alternative Care VC Deals and Dollars, US and EU1

Last year alternative care (AC) companies earned the bulk of healthtech investments, with new investors deploying record amounts of capital into the subsector and raising valuations.

Consequently, AC companies saw the sharpest decrease in investments and later-stage valuations this year.

Despite the steep drop, investment this year ($5.6B) is still well ahead of 2020’s total ($5.4B).

Investment dramatically shifted to earlier stages where valuations are lowered from 2021’s levels. Growing opportunities at the earlier stage indicate that AC companies are not slowing down.

Now that virtual care is ubiquitous in 2022, investment is shifting to companies delivering quality outcomes. Mature AC companies must not only prove their profitability but also their ability to take on risk and accountability with buyers to deliver quality outcomes.

Notes: 1) EU includes UK-based companies. Source: Pitchbook, SVB proprietary data and SVB analysis.

Virtual and hybrid care models have proven especially effective in providing high-quality primary care and mental healthcare. A recent study showed that virtual primary care increased mental health screenings and improved chronic condition management.1 These two therapeutic areas received over half of all virtual care investment in 2022.

Virtual care also provides more flexibility to physicians, improving optimism about the effects of AC on physician burnout.2 Even as virtual care continues to explode and as in-person models receive less investment, in-person will always be necessary for complex care delivery.

Focused on providing care that enables a patient to see a provider remotely

Focused on providing care that is a combination of in-person and virtual

Focused on providing care that requires the patient to physically visit a provider

Notes: 1) All 2022 data is through 9/30/2022. Source: Pitchbook, SVB proprietary data and SVB analysis.

A record number of point solution AC companies formed in 2021, creating a highly competitive landscape saturated with point solutions.

As point solutions continue to compete for the same providers and employers and point solution fatigue increases, companies will grow to integrate and expand platforms.

Many companies that started as point solutions have already evolved to offer platform care, such as Honor and Hinge Health. This can provide AC companies with additional revenue streams and improved care models, and we expect to see more of this activity in Q4’22 and 2023.

Shifts to whole-person care drove investments into primary care and platform care this year, which earned 43% of 2022 investment. Going forward, AC companies may need to prove they can integrate, scale, improve health outcomes and be profitable or reimbursable by payers.

AC Investment by Top Applications, US and EU1

$976M

54

$3.8B

101

$1.5B

60

$2.3B

59

$5.0B

94

$1.7B

51

$242M

16

$485M

32

$308M

$823M

17

$622M

8

$350M

13

$1.0B

$262M

10

Notes: 1) EU includes UK-based companies. 2) All 2022 data is through 9/30/22. 3) Platform care combines primary care with at least one form of specialty care. Source: PitchBook, SVB proprietary data and SVB analysis.

Mental health AC companies earned a record 28% of all AC dollars in 2022, up from 17% in 2020. We also saw significant interest in senior care companies, as the aging population increasingly faces complex and costly healthcare challenges.

At the early stages, we’ve seen more AC companies offering culturally centered, whole-person care. Leaders in the space include Folx Health ($25M Series A, 1/19/21), Zocalo ($7M seed round, 9/19/22) and Hurdle ($6M seed round, 1/7/21).

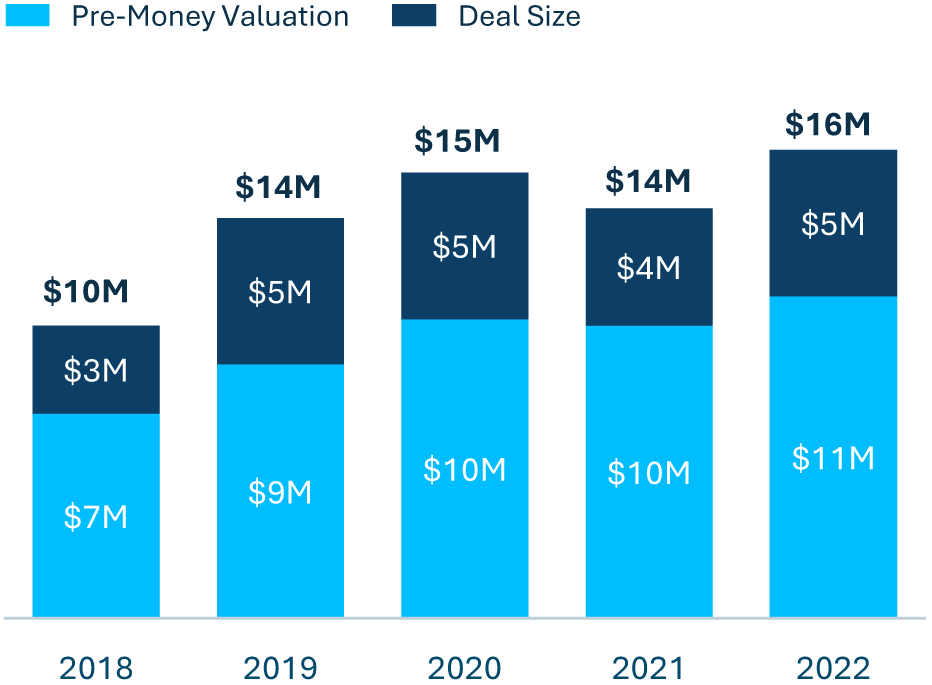

Median Series A Post-Money Valuations, US and EU2

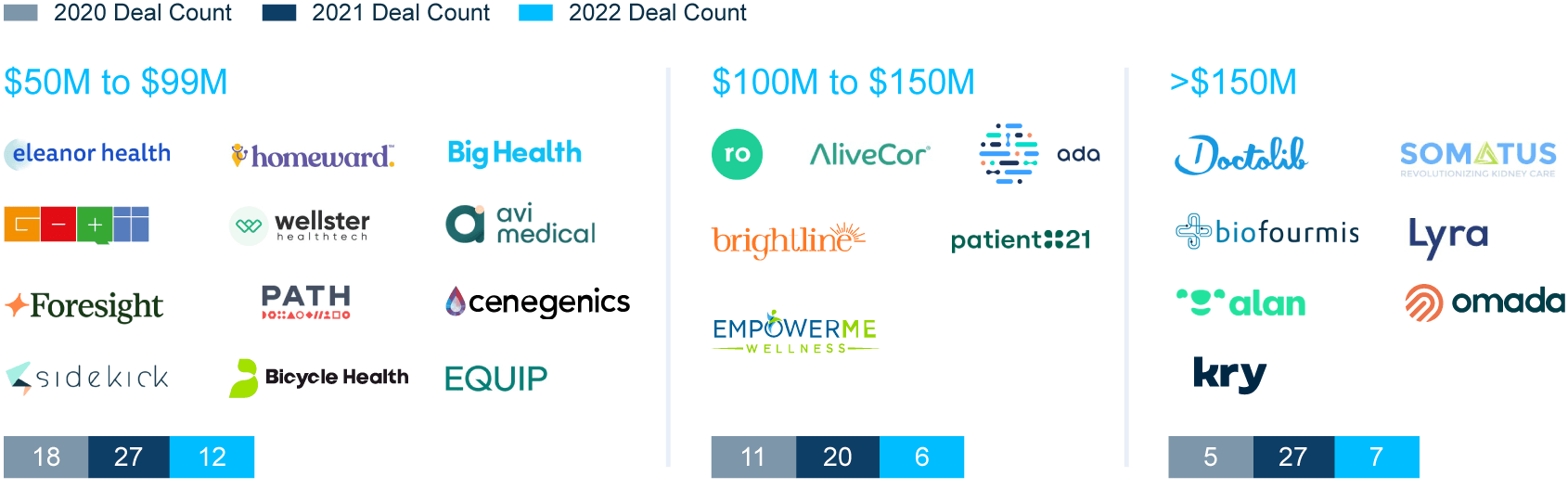

Notable 20221 Deals, US and EU2

Notes: 1) All 2022 data is through 9/30/2022. 2) EU includes UK-based companies. Source: Pitchbook, SVB proprietary data and SVB analysis.