The women’s health (WH) industry has never seen more momentum than now. This year, the largest WH devoted fund closed, early-stage investment hit a new record, and the second-ever WH unicorn (Bellabeat) was born. The overturn of Roe v. Wade in 2022 also sparked attention to WH, highlighting the necessity for WH innovation and fueling mission-driven founders to continue moving the needle.

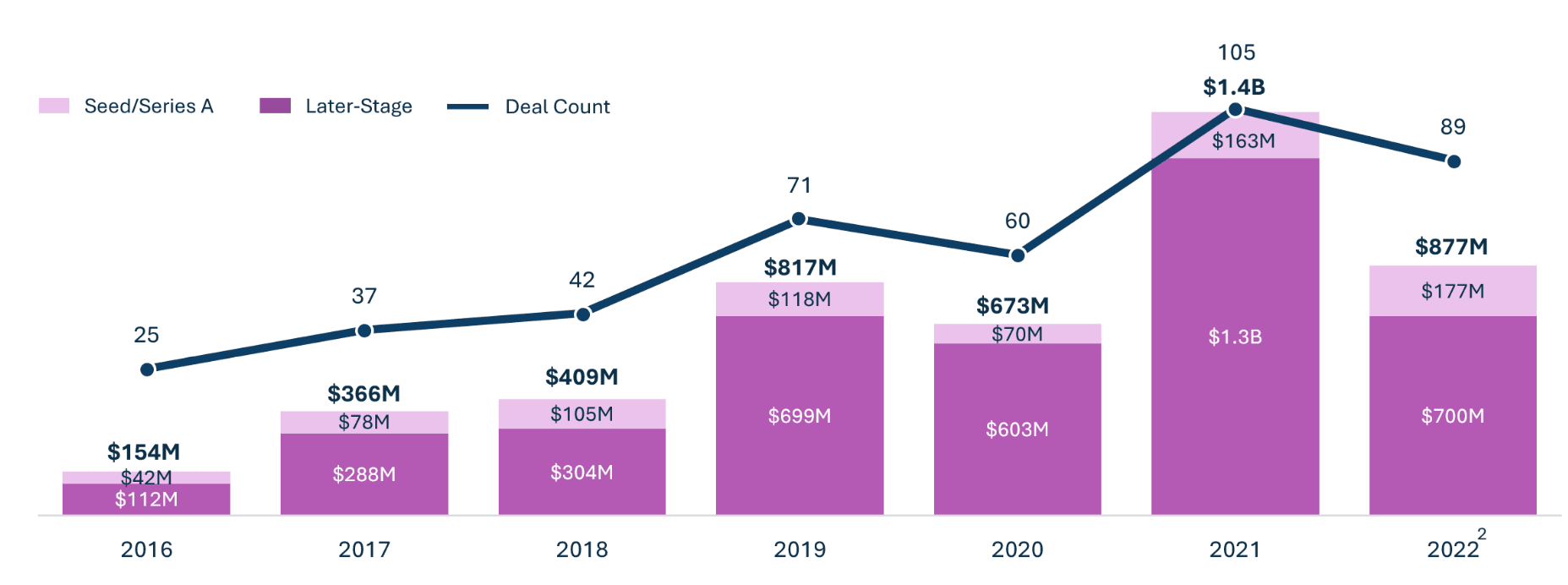

Last year, investments hit an all-time record of $1.4B. This year is slightly down from 2021 but is already 30% above 2020’s full-year investments.

We have seen investments shift to early-stage, as new entrants provided new solutions for WH challenges. Seed/Series A investments hit a record $177M in the first three quarters of this year alone, up 9% from 2021.

The increase in investments despite the market’s broader downturn is promising for the WH industry. As these companies grow and mature, they can scale to serve more women and their diverse health needs.

Notes: 1) EU includes UK-based companies 2) All 2022 data is through 9/30/22. Source: PitchBook, SVB proprietary data and SVB analysis.

"50% of the population isn’t niche,” says Maria Velissaris, founding and general partner of SteelSky Ventures. Velissaris's perspective highlights the immense opportunity WH companies hold to serve the health needs of half our population.

Platform

$1.02B

Pregnancy

$950M

Mirvie3

$155M

Fertility

$125M

$115M

Oncology

$109M

$102M

$80M

$67M

$50M

Investors will likely strike on the investment opportunities in WH as the industry continues to grow and provide new solutions for the health needs of women.

Notes: 1) Highest-valued defined by post-money valuation on private round in 2021–Q3’22. 2) EU includes UK-based companies. 3) This company overlaps with the dx/tools sector. Source: PitchBook, SVB proprietary data and SVB analysis.

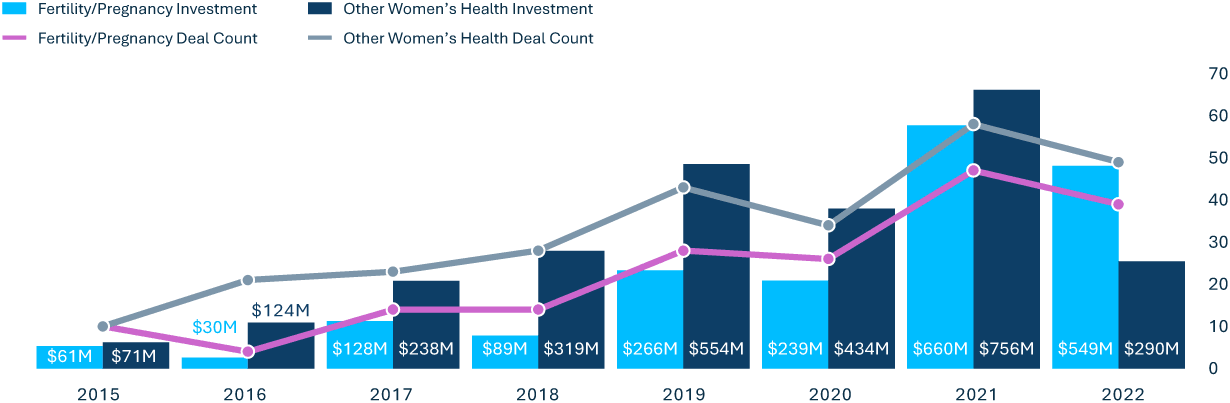

Fertility and pregnancy companies dominated WH investment in 2022, accounting for a record 68% of all investment. Historically, therapeutic areas other than fertility and pregnancy, such as pelvic floor health and menopause, have received more combined investments and have shown substantial growth.

We anticipate increased investment into therapeutic areas outside of fertility and pregnancy as they garner more attention.

We also notice several WH alternative care companies moving towards whole-person care. Maven Clinic recently announced the addition of menopause care to their platform, and Kindbody expanded their platform into women’s mental health.

Tia and Parsley Health both aim to take a holistic approach when providing care, offering gynecological services alongside primary care.

Notes: 1) Other companies are focused on single indications such as breastfeeding, mammography, women’s mental health, and breast cancer. 2) EU includes UK-based companies. All 2022 data is through 9/30/22. Source: PitchBook, SVB proprietary data and SVB analysis.

Investment by Application, US and EU1

2020

2021

20222

Applications

Dollars

Deals

$107M

13

$211M

22

$253M

$132M

12

$448M

25

$296M

27

15

$508M

17

$75M

14

Menopause

$57M

4

$16M

6

$46M

Pelvic Health

$89M

9

$53M

$76M

$0

0

$12M

5

$79M

10

Birth Control

$11M

3

$63M

7

$5M

2

Menstruation

$9M

$94M

$2M

Notes: 1) EU includes UK-based companies. 2) All 2022 data is through 9/30/22. Source: PitchBook, SVB proprietary data and SVB analysis.

These new models applied in fertility and pregnancy are improving maternal health outcomes by increasing access to specialty providers, including OBGYNs, nutritionists, and mental health providers.

Companies focusing on hormone health are increasing productivity in women who suffer from debilitating and historically undiagnosed hormone-related conditions.

We predict that personalized, whole-person care will continue to grow, as WH is not a one-size-fits-all solution.

These companies are not only serving 50% of the population, but are also helping to reduce stigmas, raising awareness, and dismantling the taboo culture around WH.

Largest 20221 Deals by Indication

Notes: 1) All 2022 data is through 9/30/22. 2) These companies overlap with the biopharma, device or dx/tools sectors. Source: PitchBook, SVB proprietary data and SVB analysis.