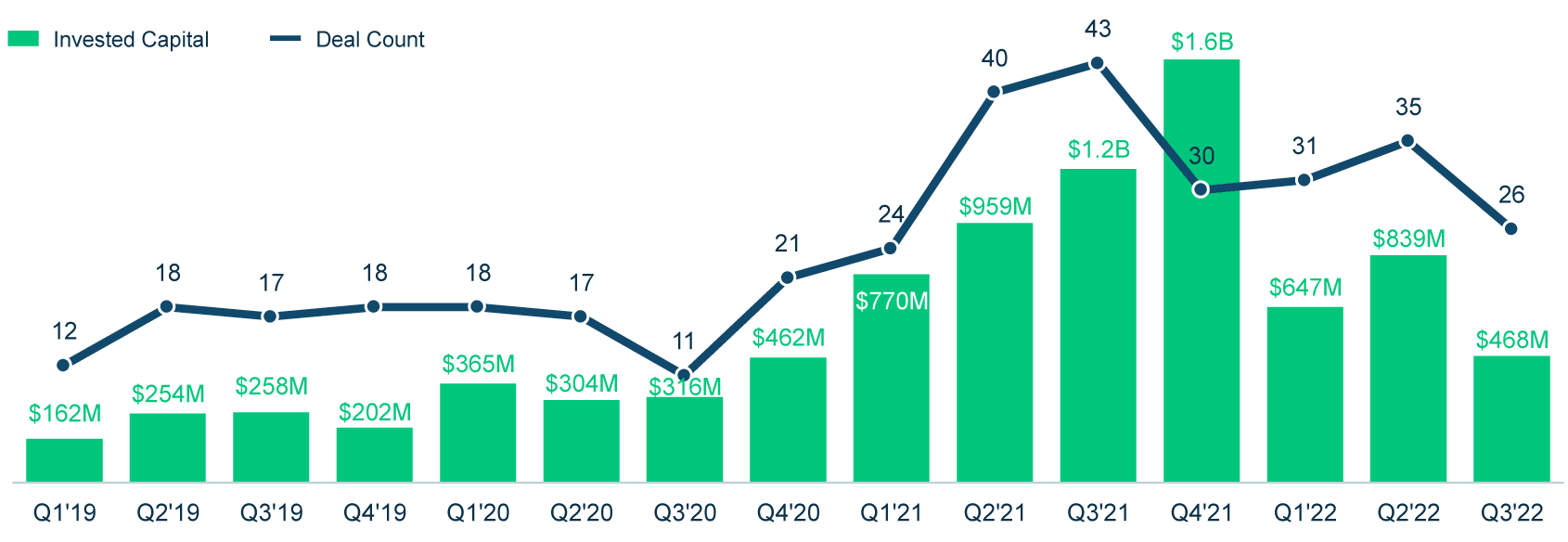

Mental health1(MH) companies weren’t immune to the market downturn this year, with investment slowing from 2021’s blockbuster levels.

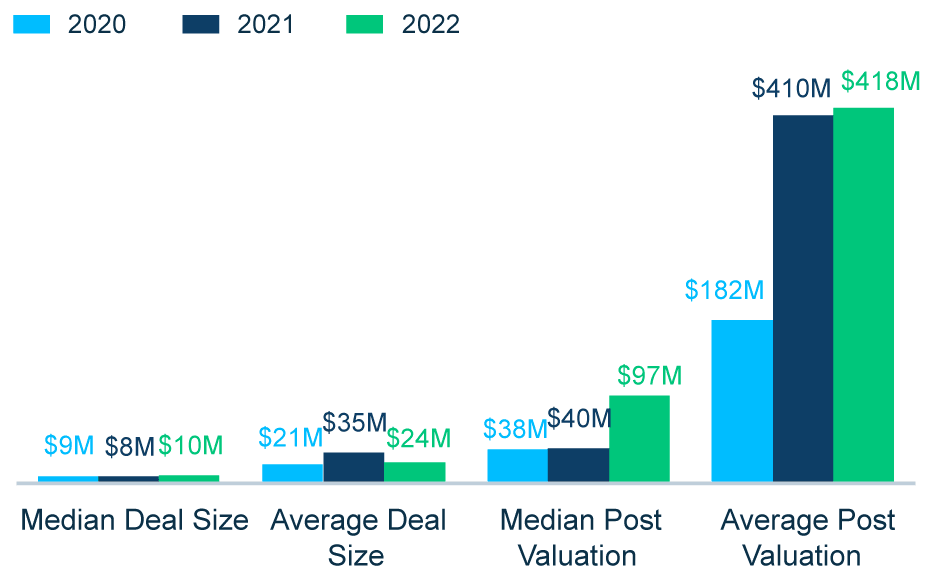

However, while the broader healthtech industry saw median deal sizes and valuations decrease in 2022, MH companies actually saw increases.

Many MH solutions rapidly expanded and scaled their platforms this year, enabled by record amounts of capital deployed to them in 2021.

As a result, employee-sponsored MH benefits have shifted from a nice-to-have to a must-have. They’ve improved accessibility and gained traction among employees, with high engagement rates and promising outcome improvements. Demand for these solutions continues to grow, providing opportunities for MH companies to expand.

Market leaders in MH are also assuaging the provider shortage, which has reached a tipping point.2

Notes: 1) This analysis does not include the $2B raised this year (as of 9/30/22) by healthtech companies with mental health offerings that are not exclusively focused on mental health. 2) AAMC report. 3) EU includes UK-based companies. Source: PitchBook, SVB proprietary data and SVB analysis.

The hybrid care model in particular has exploded in popularity, as in-person care remains the most trusted by patients while virtual options improve access and offer more touchpoints at lower costs.

As demand continues to soar and MH tops concerns of consumers, employers, investors, payers, and providers, we believe MH investment will remain steady in 2023.

Notes: 1) EU includes UK-based companies, 2) All 2022 data is through 9/30/22. Source: PitchBook, SVB proprietary data and SVB analysis.

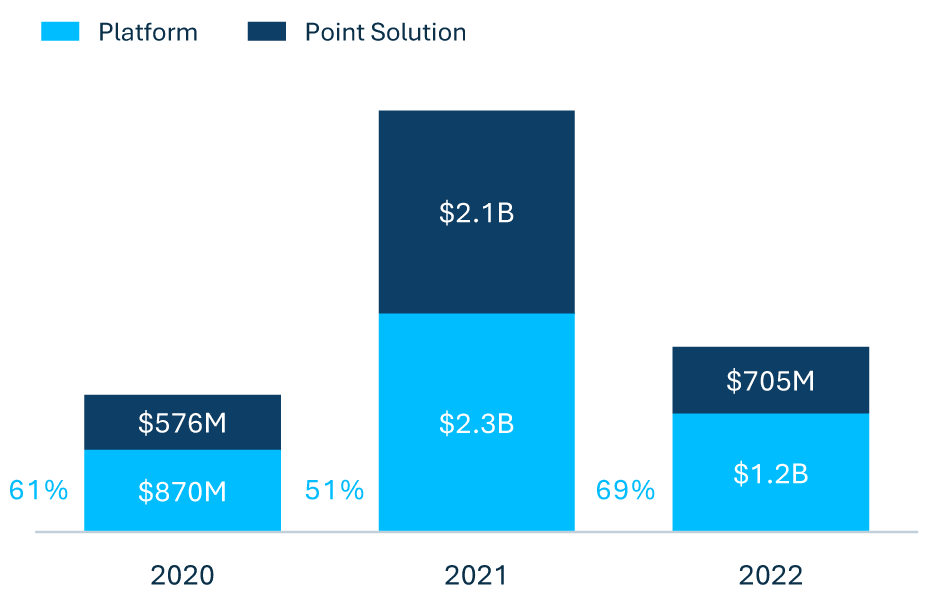

Last year saw a sharp rise in investments into point solution3 companies focusing on a single MH disorder. This created a highly competitive landscape saturated with point solutions.

Since then, we’ve seen many point solutions evolve into platform4, expanding service offerings to other areas of MH. Platform solutions dominated MH this year, earning 69% of investments, up from 51% last year.

As MH care demand soars, we expect more point solutions to expand to platform to grow their patient bases. Despite market saturation, point solution valuations have risen in 2022. Their focus on single conditions allows for high-quality, specialized healthcare, especially for higher-acuity MH disorders like treatment-resistant depression, OCD, etc. Interestingly, point solution median deal size in 2022 ($12M) is double platform’s ($6M).

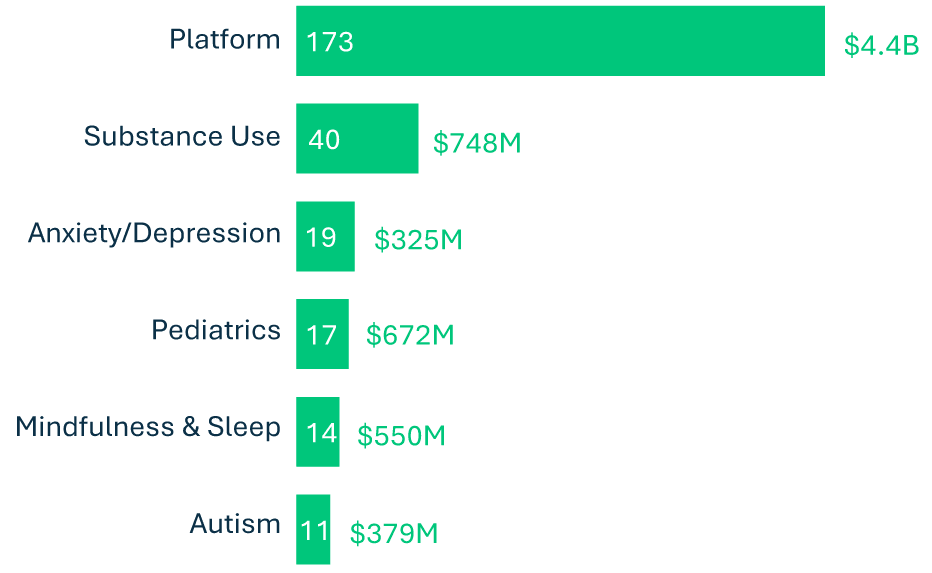

We’ve also seen an increase in culturally competent MH services that meet the social, cultural, and linguistic needs of patients. For example, the Bronx-based company Health in Her Hue connects Black women to appropriate healthcare providers, including MH providers.

Going forward, we expect to see more companies expand access to culturally-competent MH care.

Notes: 1) EU includes UK-based companies. 2) All 2022 data is through 9/30/22. 3) Point solution defined as companies focused on single indication or disorder. 4) Platform solution defined as companies that target a combination of mental and behavioral health conditions. Source: PitchBook, SVB proprietary data and SVB analysis.

Notable 20221 Point Solution Deals

Notes: 1) All 2022 data is through 9/30/22. Source: PitchBook, SVB proprietary data and SVB analysis.