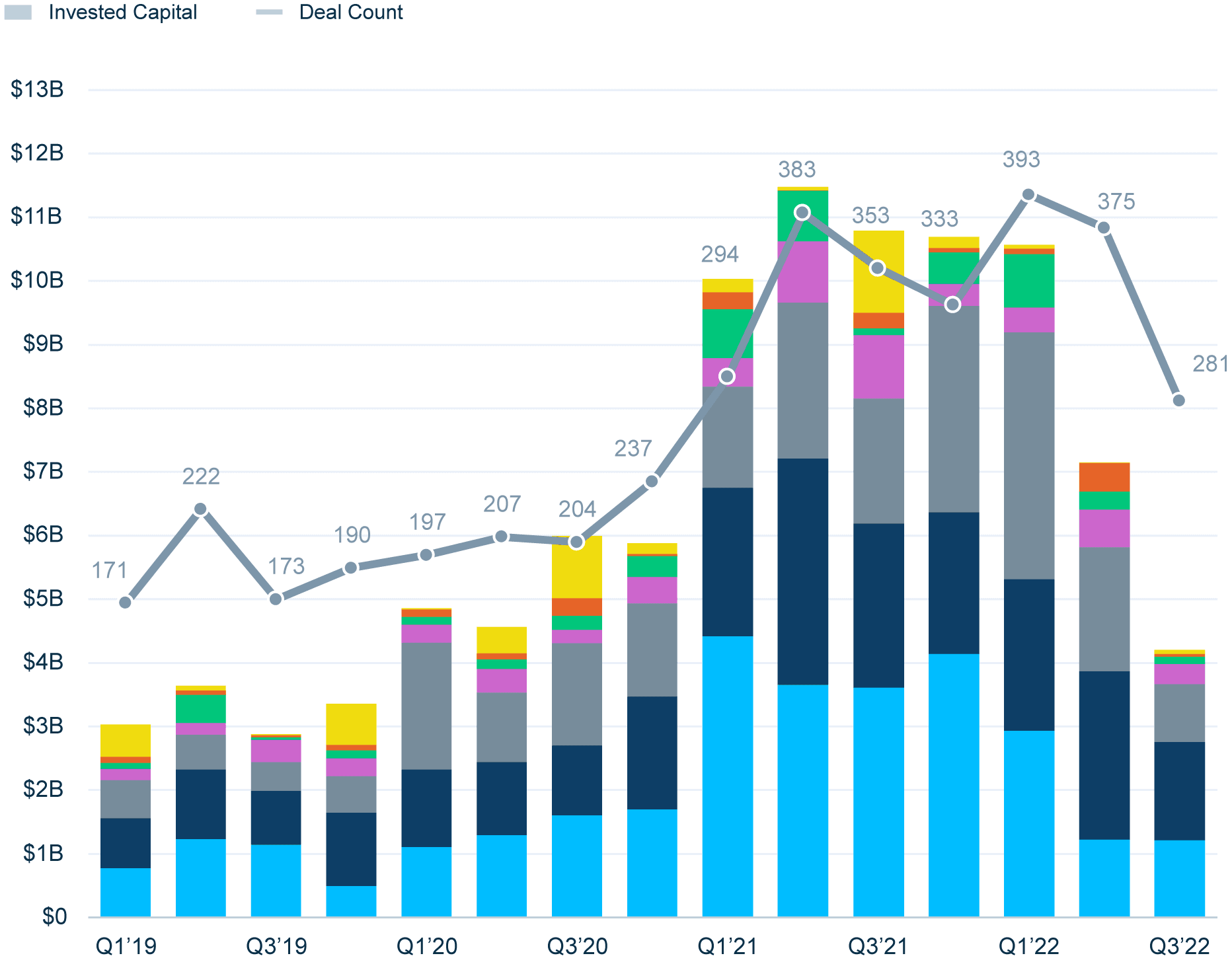

Healthtech investment and deal pace is down this year from its unprecedented levels in 2021. This downturn is expected, as the market rebalances from 2021’s unsustainable activity.

Last year, robust private and public equity markets, peaked VC fundraising and new investors pouring capital into healthtech at record rates pushed investments and valuations to all-time highs.

This year, tumultuous public markets, global geopolitical factors and rising interest rates all rebalanced healthtech investment, with an especially sharp drop in Q3’22 ($4.4B), down 39% from Q2’22 and down 67% from its peak in Q2’21.

Now, we are seeing investments shift to high-quality companies that are improving health outcomes, access or affordability. There is also a shift to earlier stages where valuations are normalized. At the later stages, valuations are correcting for companies that haven’t yet grown into their inflated valuations.

Notes: 1) EU includes UK-based companies. Source: PitchBook, SVB proprietary data and SVB analysis

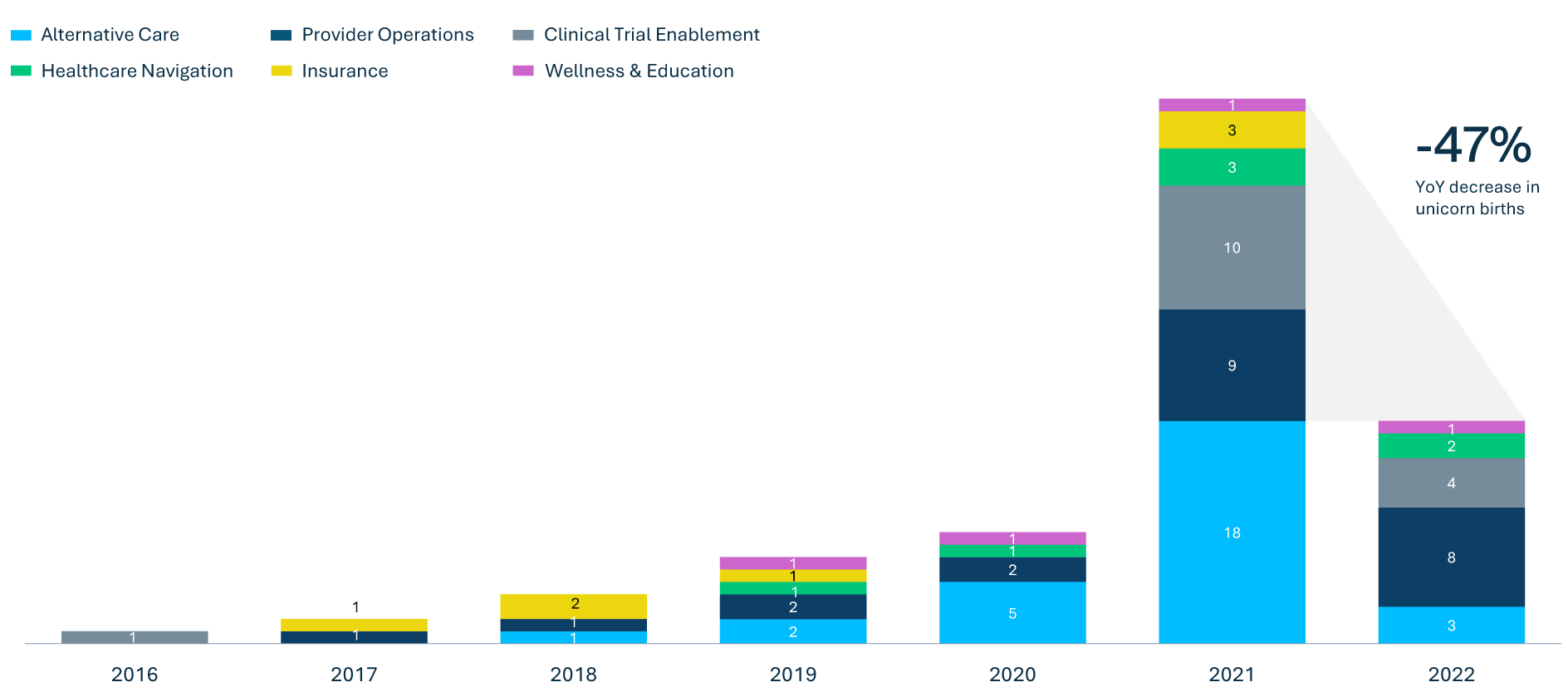

Later-stage companies are generally closing fewer deals at lower valuations, marked by a 40% decrease in mega-deal investments from 2021 to 2022. With a record amount of dry powder available to healthtech startups, there is still a tremendous opportunity for healthtech companies to grow.

We estimate that US and EU healthtech investment will reach $27B in 2022.

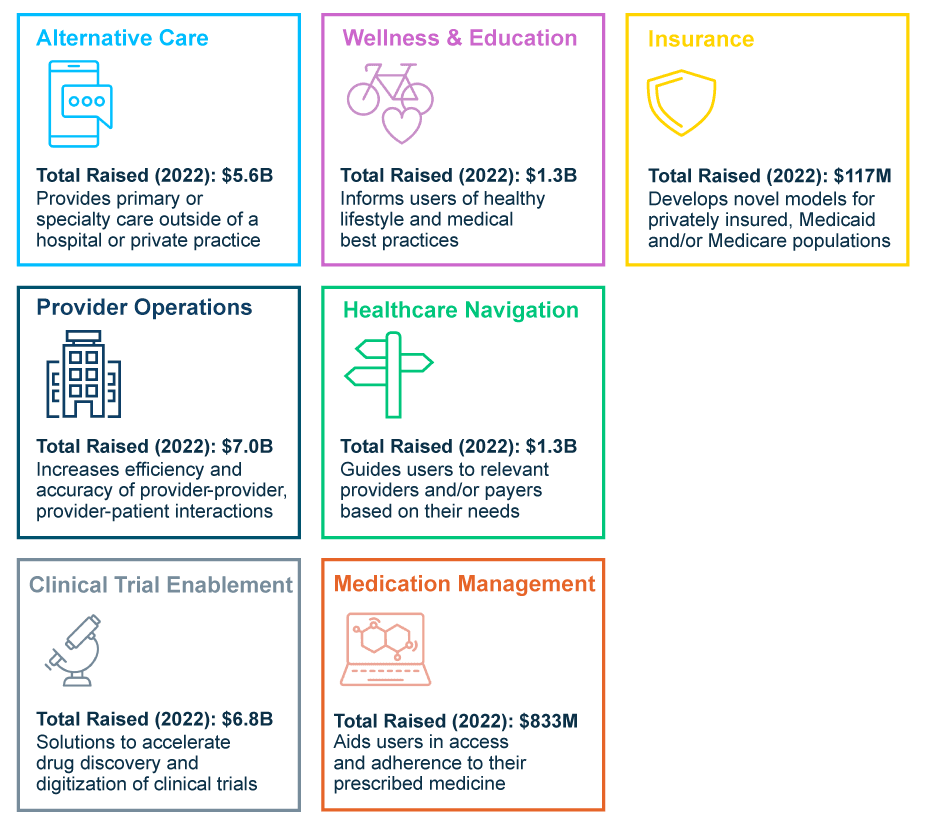

Healthtech VC Dollars by Geography

Geography

2019

2020

2021

20222

US

$11.4B

$19.4B

$39.2B

$18.6B

EU1

$2.0B

$2.2B

$4.7B

$4.1B

Total

$13.4B

$21.6B

$42.9B

$22.7B

Notes: 1) EU includes UK-based companies. 2) All 2022 data is through 9/30/2022. Source: PitchBook, SVB proprietary data and SVB analysis.

Notes: 1) EU includes UK-based companies. Source: PitchBook, SVB proprietary data and SVB analysis.

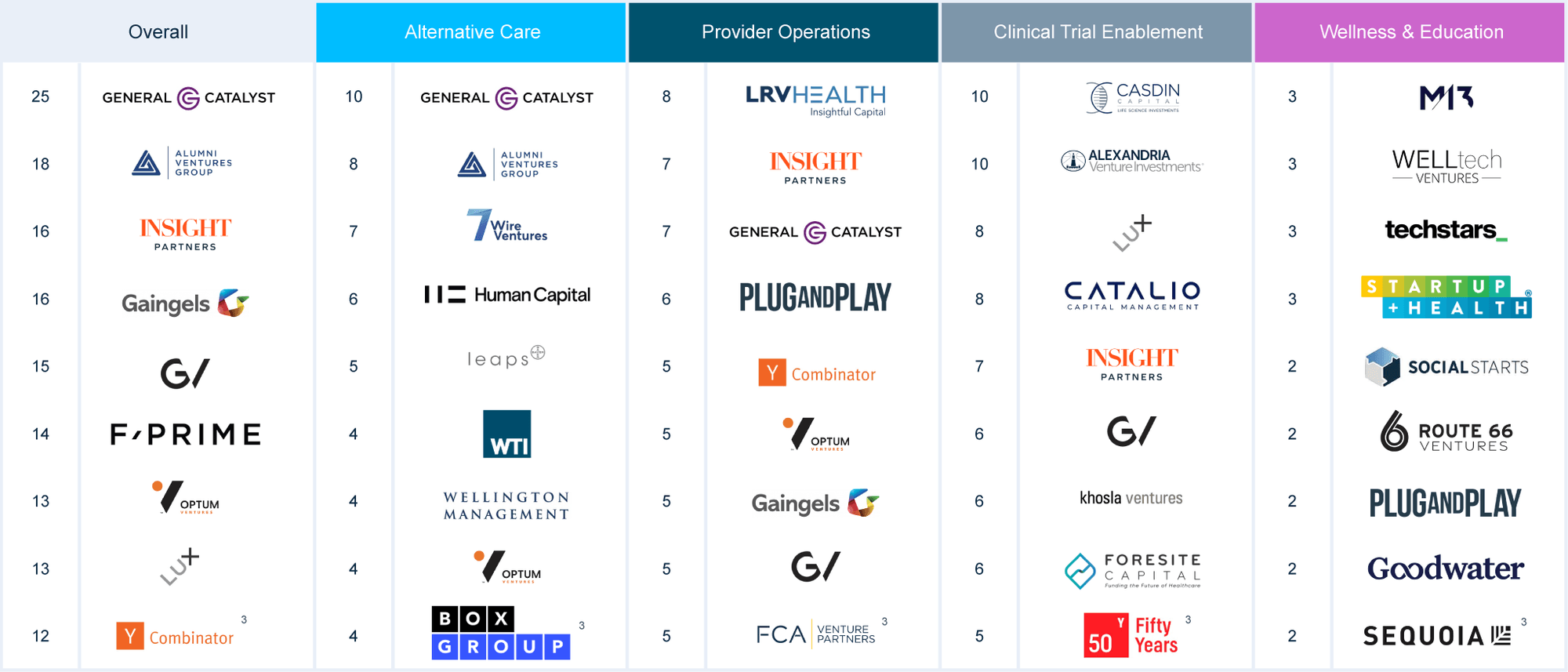

Notes: 1) Most active investors defined as by count of deals in which investor participated (new or follow-on). 2) All 2022 data through 9/30/22. EU includes UK-based companies. 3) Additional investors have the same number of deals but are not included because of space limitations. Source: PitchBook, SVB proprietary data and SVB analysis.

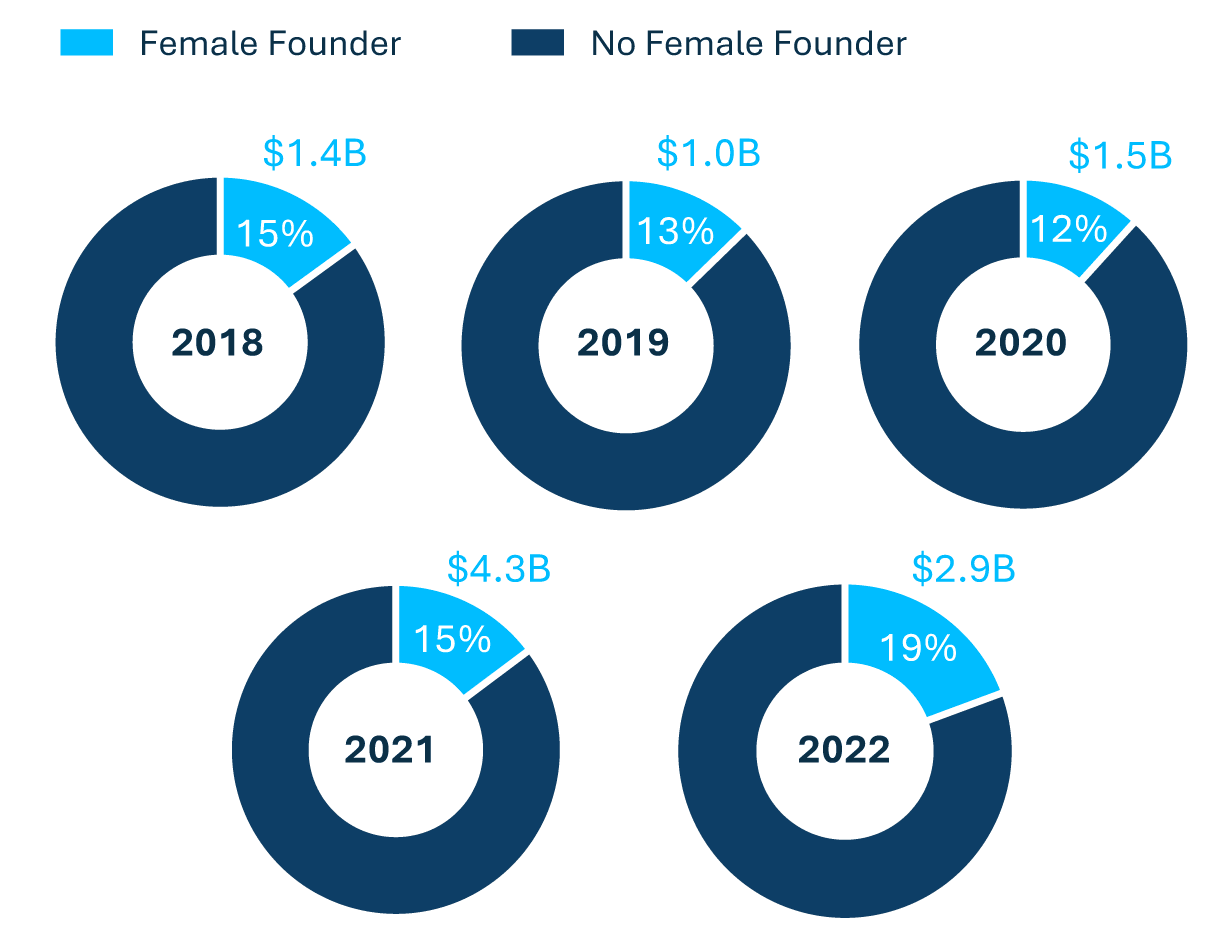

Female-founded1 healthtech companies broke a record in 2022, receiving 19% of all capital invested. This is ahead of VC investment across other healthcare sectors (biopharma, dx/tools, device), where only 12% went to female-founded companies.

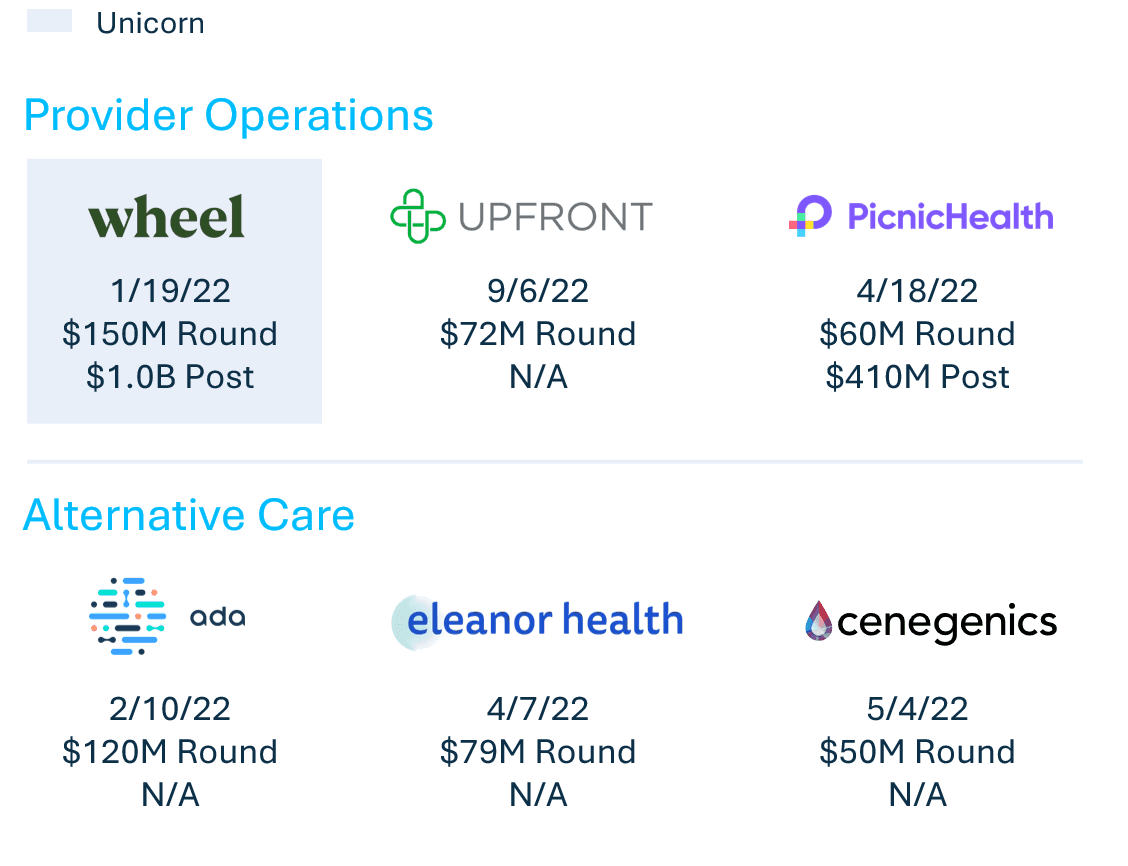

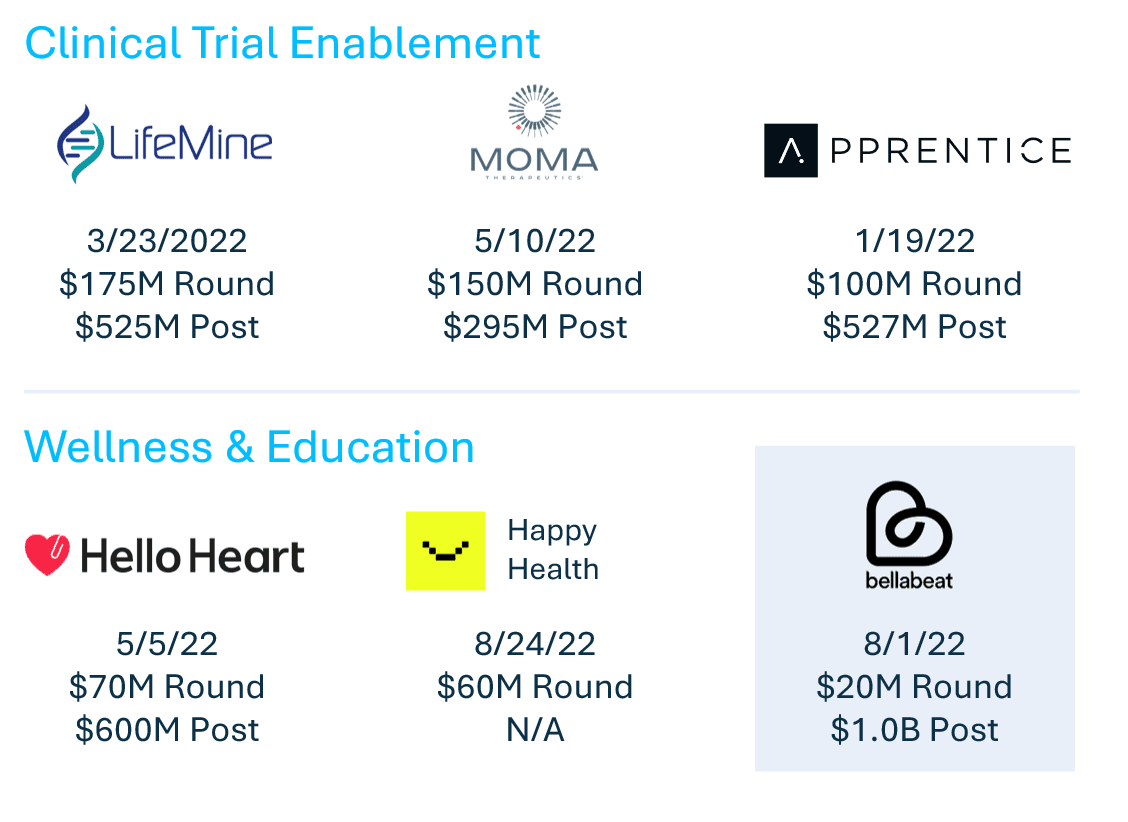

Female-founded companies are becoming more prevalent, and their valuations are increasing. Two companies in 2022 hit unicorn status (Bellabeat and Wheel).

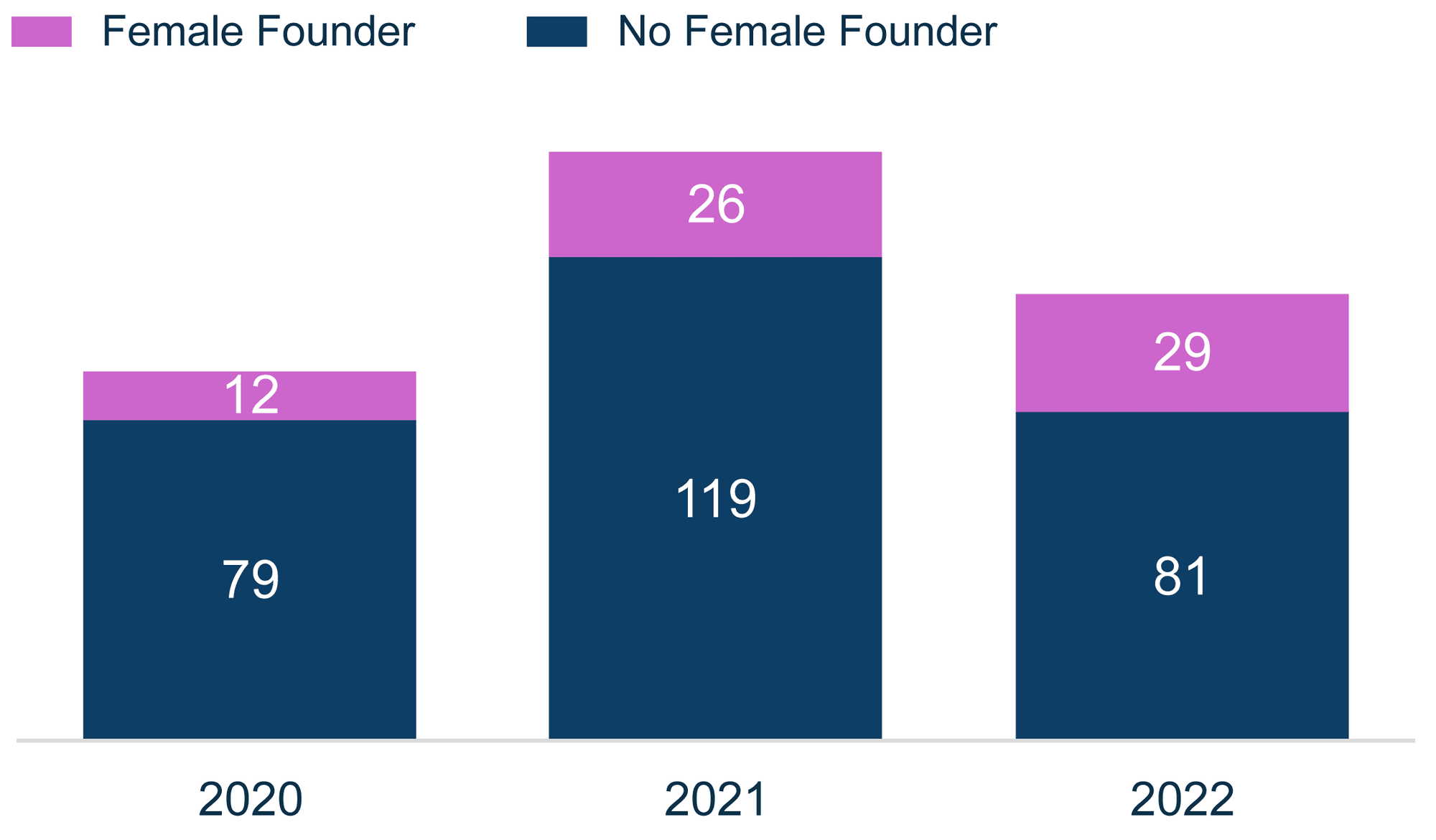

While overall healthtech valuations are down from their peak in 2021, there were more female-founded companies valued over $100M in 2022 (29 companies), a 12% increase over 2021.

Notes: 1) Female-founded companies refer to companies with at least one female founder. 2) EU includes UK-based companies. All 2022 data is through 9/30/22. Source: PitchBook, SVB proprietary data and SVB analysis.

The higher concentration of female founders among the highest-valued healthtech companies is a promising development for the industry.

Increasing perspectives and the pool of knowledge due to diversity will create better solutions to healthcare’s toughest problems. Women can not only provide unique lenses to these challenges, but can also strongly identify with female consumer bases.

With VCs now holding record amounts of dry powder following a record fundraising season, it is crucial that investors consider diverse founders and challenge traditional funding inequities.

Note: 1) ) EU includes UK-based companies. All 2022 data is through 9/30/22. Source: PitchBook, SVB proprietary data and SVB analysis.

Note: All 2022 data is through 9/30/22. Financing date, size and post-money valuation listed when available. Source: PitchBook, SVB proprietary data and SVB analysis.

Notes: 1) All 2022 data is through 9/30/2022. Source: PitchBook, SVB proprietary data and SVB analysis.

Note: 1) EU includes UK-based companies. 2) All 2022 data is through 9/30/22. 3) De-SPAC is a company merger of the special purpose acquisition company (SPAC), the buying entity and a target private business. Source: PitchBook, SVB proprietary data and SVB analysis.

Note: 1) EU includes UK-based companies. 2) All 2022 data is through 9/30/22. Source: PitchBook, SVB proprietary data and SVB analysis.