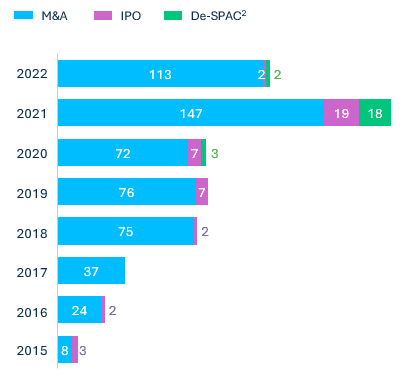

Healthtech’s IPO window shut this year, marking an end to the wave of new listings from 2019-2021. This year’s IPOs, both in Q3, were international provider operations companies ClouDr and Lunit, based in Hong Kong and South Korea, respectively.

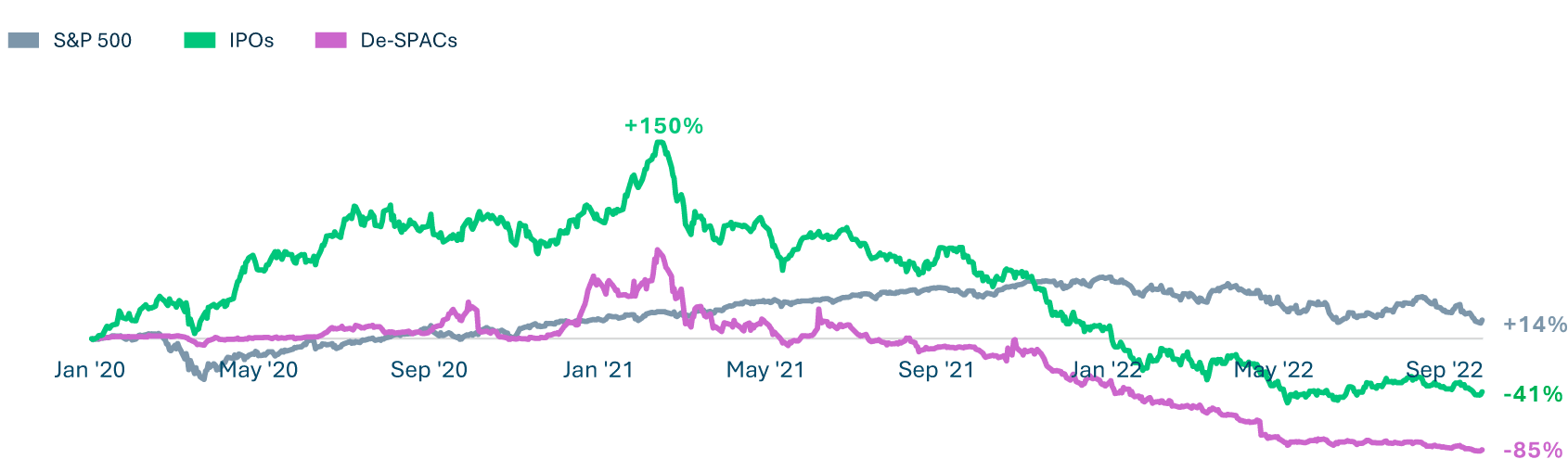

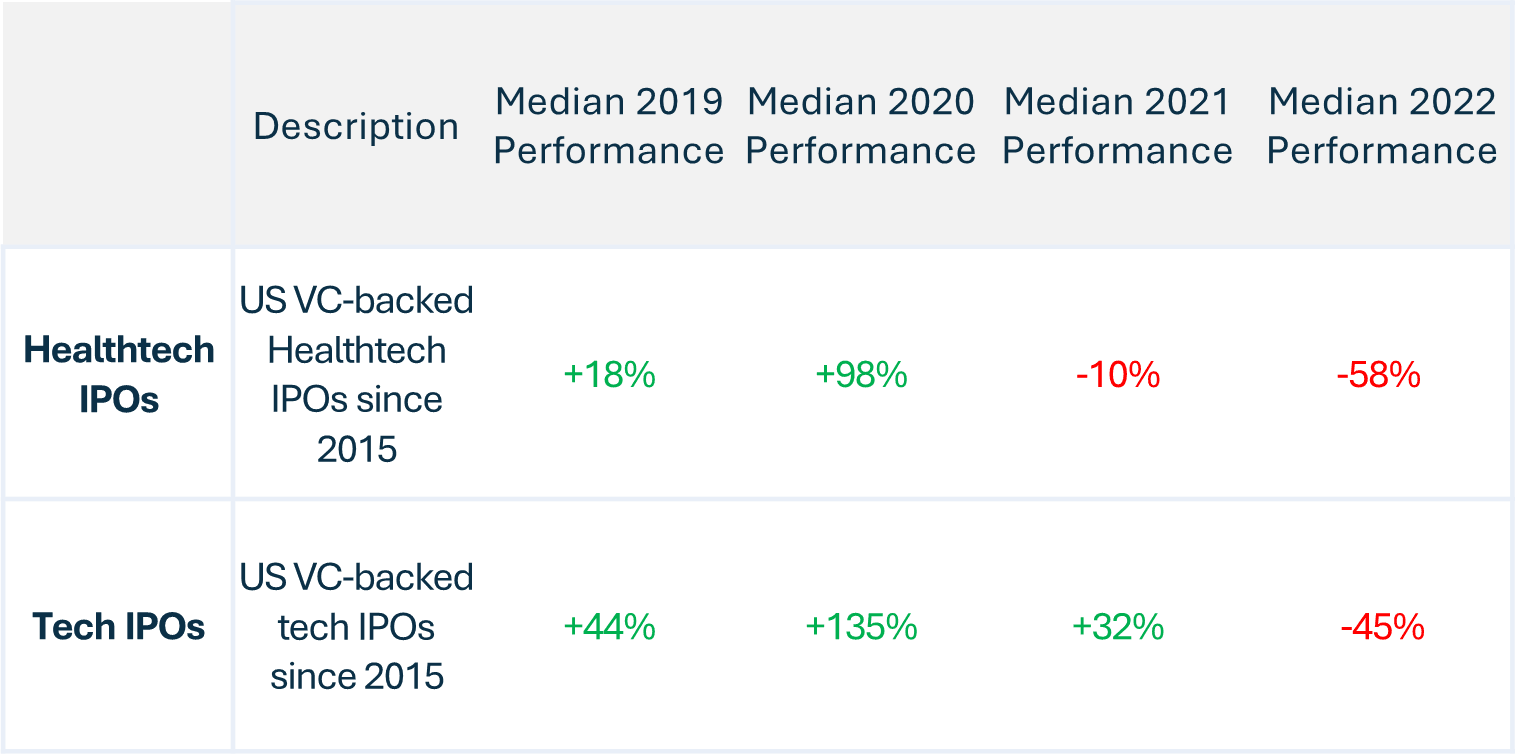

Inflation, supply chain constraints, interest rate hikes and the situation in Russia and Ukraine all contributed to the stock market’s worst first half since 1970. The volatility hurt performance across all sectors, but especially in healthtech, with median 2022 performance at -58%.1

Despite last year’s influx in healthtech IPOs, the end-of-year 2021 performance was disappointing, with the majority of healthtech stocks trading negatively. This revealed the public market’s dissipating enthusiasm for tech-enabled healthcare growth stories.

Notes: 1) IPO data only includes venture-backed IPOs since 2015 with minimum $25M proceeds raised. 2) De-SPACs graphed by date of announcement of intent to de-SPAC. 3) Performance measured by change in index value as of 1/1/20. All 2022 data is through 9/30/22. Source: S&P Capital IQ, PitchBook, SVB proprietary data and SVB analysis.

Public performance of VC-backed unicorns born in 2015-2021 was mostly negative in 2021, with all trading negatively except One Medical (+45%) and Health Catalyst (+92%). This year, performance worsened with only One Medical (+22%) trading positively following Amazon’s announcement to acquire the company.

SPACs, which exploded in popularity last year, seem to have fallen out of vogue, with all trading negatively. Median de-SPAC performance since merger close reached a record low in Q3’22 (-80%), down significantly from 2021 (-35%). As uncertain market conditions continue, we expect healthtech companies to remain private and delay IPO plans, while considering M&A opportunities.

Notes: 1) IPO data only includes venture-backed IPOs since 2015 with minimum $25M proceeds raised. Source: S&P Capital IQ, PitchBook, SVB proprietary data and SVB analysis.

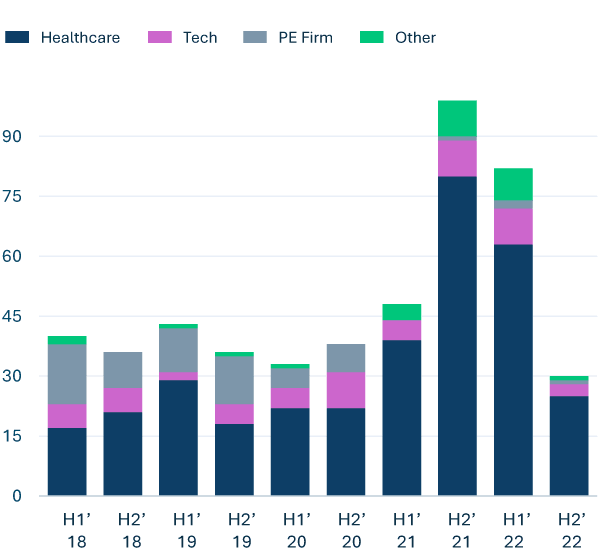

M&A deal activity in healthtech this year started strong in Q1 (48 deals) but tapered off in Q2 (33) and Q3 (30), with Q3 down 44% from the peak in Q4'21 (54). We expect M&A volume to be slightly down in Q4'22, with yearly totals behind 2021’s record pace.

While M&A activity tapered slightly, median acquisition prices were significantly down. Acquirers struggled with valuation disconnect, driven by big step-ups and resulting lofty post-money valuations we saw with regularity in 2020 and 2021.

Deal pricing will likely remain unsettled as private valuations correct. This is playing out in 2022 as median later-stage post-money valuations ($100M) are down 17% from their peak in Q4 2021 ($121M), while public market healthtech market caps continue to drop below pre-record 2021 levels.

There were only six publicly disclosed private healthtech M&As in 2022 over $50M and zero over $1B (2021 had four). M&A in 2021 boasted strong return multiples2 for many of the disclosed deals; however, in 2022 public market corrections have impacted return multiples for investors, as two of the six (Analytic Wizards and PlusDental) seemed to have larger prior private round post-money valuations than exit values.

Notes: 1) M&A data only includes private, venture-backed M&A. All 2022 data is through 9/30/22. Source: PitchBook, SVB proprietary data and SVB analysis.

Notes: 1) M&A data only includes private, venture-backed M&A. All 2022 data is through 9/30/22. 2) Return multiple defined as the acquisition price divided by the post-money valuation on the prior private round. Source: PitchBook, SVB proprietary data and SVB analysis.

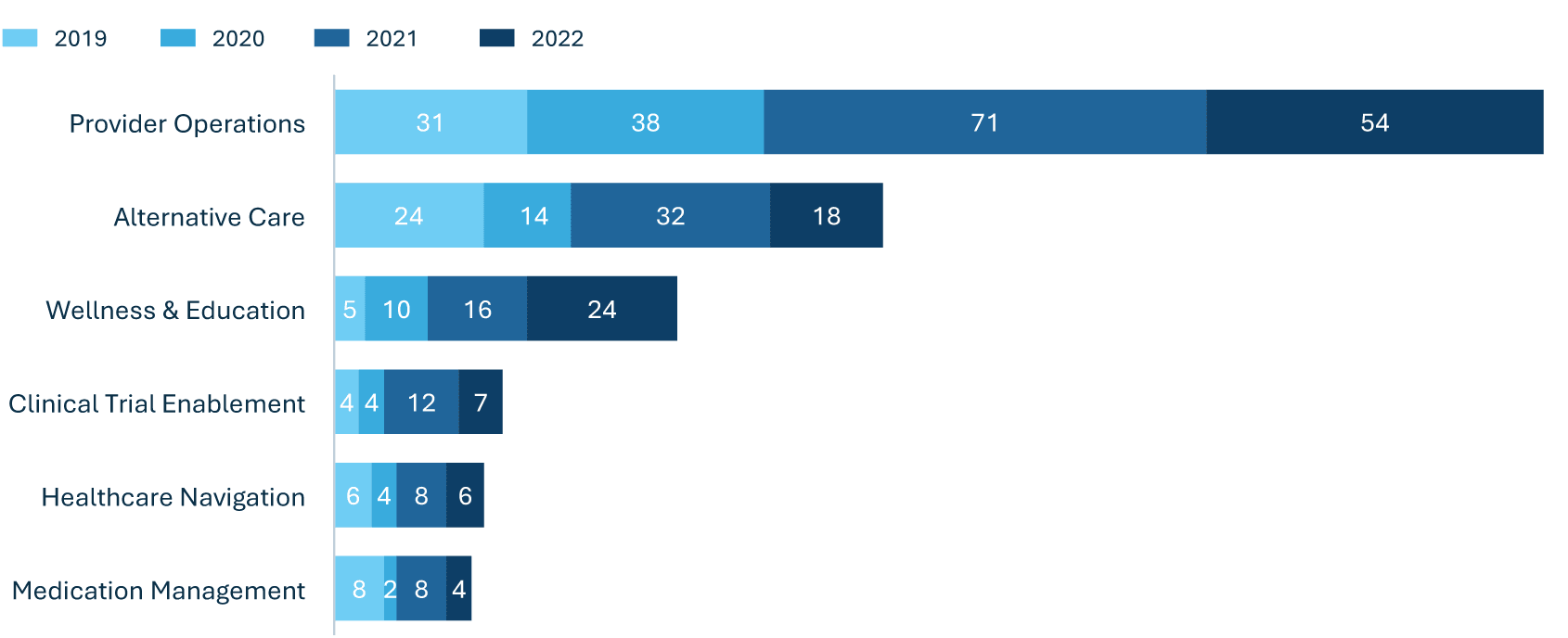

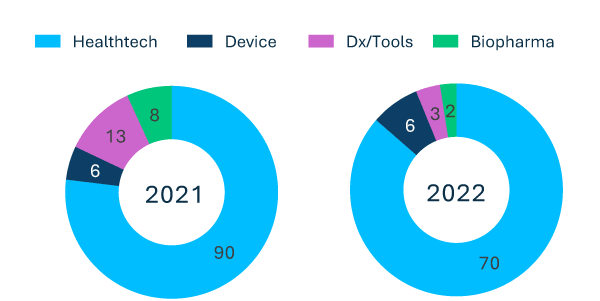

Public healthcare companies lead private M&A activity in 2022, while acquisitions by PE firms have continued to decline since early 2021. Healthtech companies acquired the most of any other healthcare sector (biopharma, diagnostics, and device), with 70 acquisitions (86% of healthcare acquirer activity and 63% of overall activity) in 2022.

We expect well-positioned private healthtech companies, flush with cash on their balance sheets from 2021 mammoth rounds, to continue to be opportunistic acquirers in the space in Q4'22 and 2023.

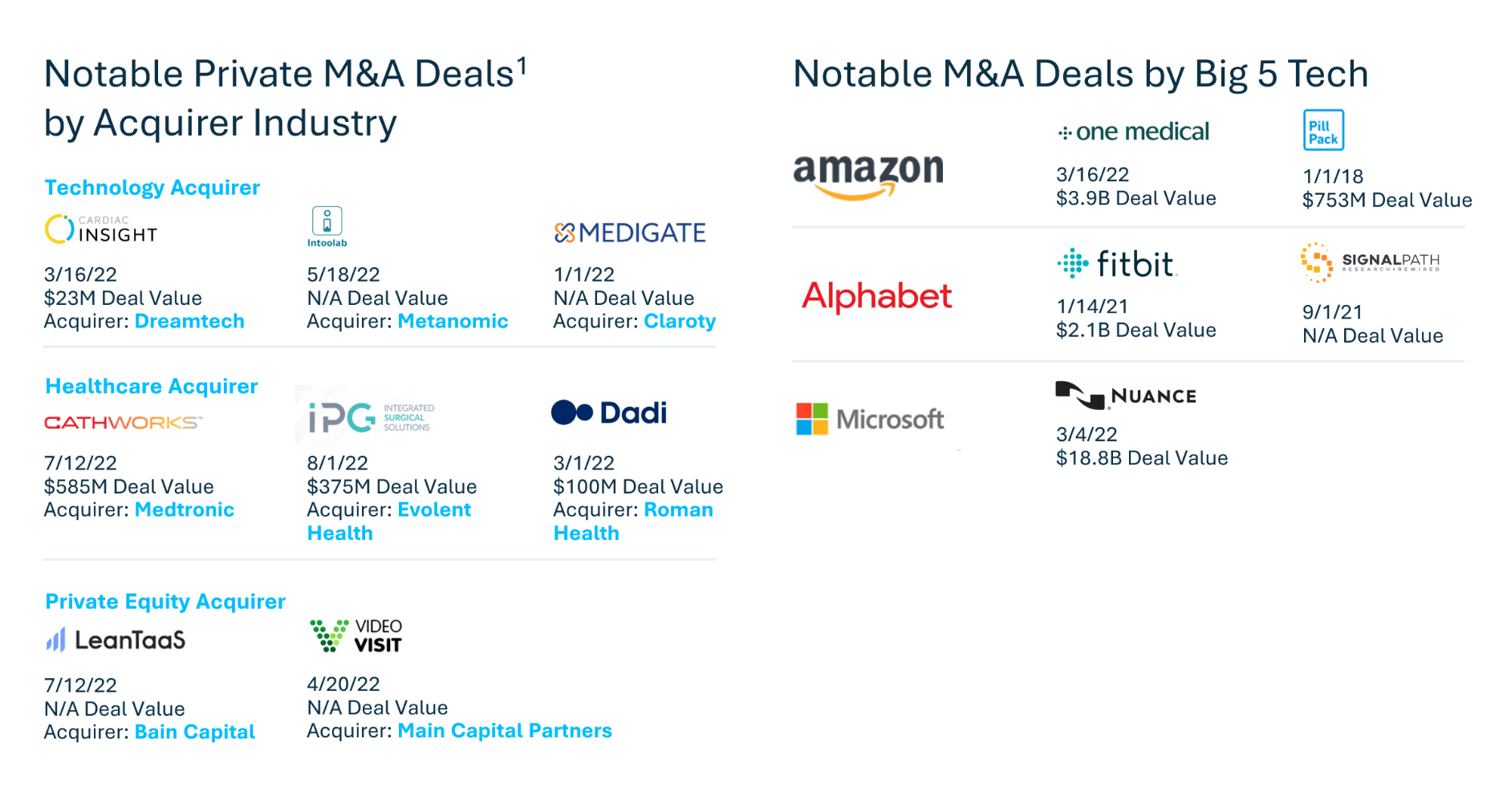

This year saw some notable public M&A activity by Big 5 tech companies: Amazon (One Medical) and Microsoft (Nuance Communications). We believe large technology companies, equipped with technology, data and cash, will continue to venture into the healthcare industry, as it remains highly challenged and ripe for innovation.

Various industry factors lead us to believe M&A will remain steady. Healthcare acquirers can leverage growth-stage companies’ technology to build stronger relationships with providers and provide better navigation for patients. We expect a wave of consolidation in the next three quarters with a broad range of acquirers including large technology companies.

Notes: 1) M&A data only includes private, venture-backed M&A. All 2022 data is through 9/30/22. Source: PitchBook, SVB proprietary data and SVB analysis.

Notes: 1) M&A data only includes private, venture-backed M&A. Source: PitchBook, SVB proprietary data and SVB analysis