As healthtech investor focus shifted to quality and outcomes this year, health & wellness (H&W) investment focused on companies offering improved healthcare outcomes. These companies often pair a user-friendly consumer application with devices or diagnostic tests.

As H&W companies shift their focus to improving outcomes, we’ve seen some of these companies evolve into the clinical space. For example, mindfulness app Headspace expanded their platform by acquiring Ginger, a therapy provider, for $3B in 2021.

H&W companies are also shifting away from direct-to-consumer (D2C) models to business-to-business (B2B) models. With consumer inflation at all-time highs, and digital customer acquisition costs skyrocketing, competition to capture consumer dollars is high.

Shifting to B2B and business-to-consumer (B2C) paves paths for H&W companies to scale engaged customer bases by working within existing healthcare system infrastructures, and acquiring consumers through health systems, payers and employers.

Notes: 1) EU includes UK-based companies. Source: PitchBook, SVB proprietary data and SVB analysis.

In 2021, many new investors entered the H&W space as the pandemic substantially increased the prioritization of wellness by consumers across the globe. Interestingly, new investor activity in 2022 was sustained, with 72% of investors into H&W companies in 2022 being new to the company.

Consumerization of healthcare has grown significantly in 2022. As H&W companies lead the shift in focus to the consumer experience, we predict there will be an even stronger consumer presence shaping the healthcare landscape in 2023.

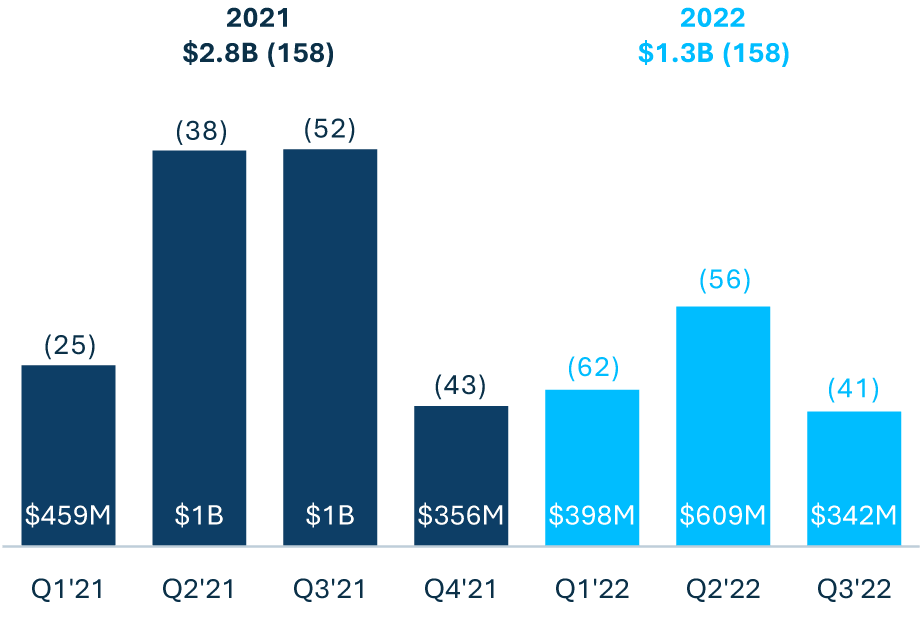

Notes: 1) EU includes UK-based companies. 2) All 2022 data is through 9/30/22. Source: PitchBook, SVB proprietary data and SVB analysis.